Your credit score can determine whether you get approved for an apartment, how much you pay upfront, and even which rental options are available to you. But what credit score is needed to rent an apartment? While some landlords have strict credit requirements, others consider additional factors like income and rental history. This article is everything you need to know to get approved, no matter where your credit stands!

What is Credit Score?

A credit score is a number that shows how reliable you are when it comes to paying back money. When you're looking to rent a home or apartment, landlords often check your credit score to get an idea of how responsible you are with your finances.

A credit score tells landlords if you usually pay your bills on time, how much debt you have, and how well you manage your credit.

What Credit Score Is Needed to Rent an Apartment?

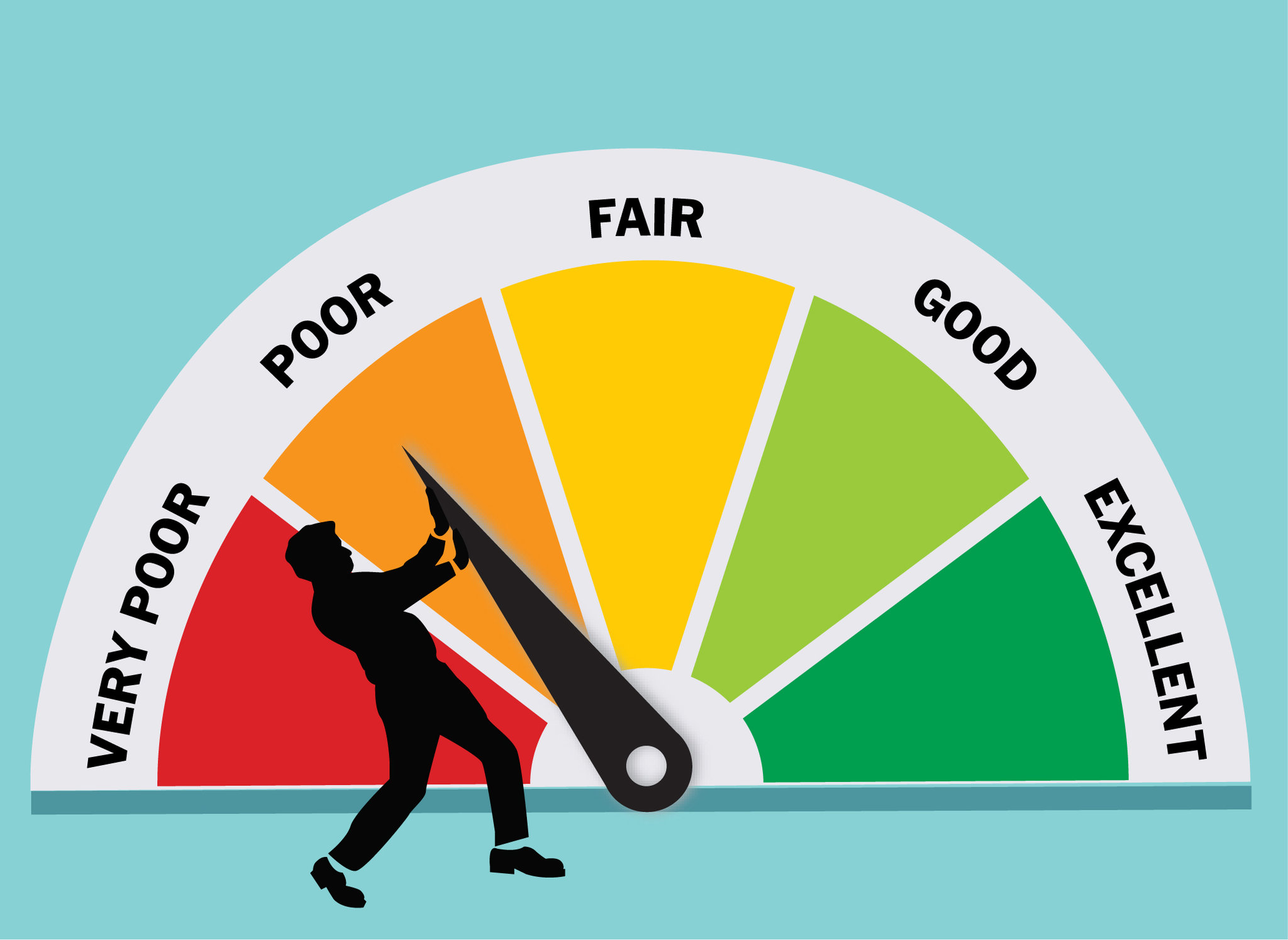

A credit score plays a key role in securing an apartment. While there’s no universal minimum, most landlords and property managers prefer a score of at least 620-650. Some accept lower scores, especially for private rentals, while high-end apartments may require 700 or above.

Landlords use credit score for apartment approval to assess financial responsibility, but other factors like income, rental history, and references also influence decisions.

Why Do Landlords Check Credit Scores?

Landlords check credit scores to evaluate a potential tenant's financial responsibility and likelihood of paying rent on time, as renting out a property involves financial risk.

A history of late or missed payments can signal a higher risk to landlords, making tenants with a record of on-time payments more likely to be approved for a lease without additional conditions. Also, credit scores reflect financial responsibility; tenants with high levels of outstanding debt relative to their income may raise concerns regarding their ability to afford rent, indicating potential financial strain.

Furthermore, a higher credit score can lead to better lease terms, such as lower security deposits or more flexible payment options. In contrast, tenants with lower credit scores might face larger deposits, the need for a co-signer, or be required to provide further proof of income to secure a lease.

What Factors Influence Credit Scores?

Your credit score is calculated based on several key factors that give a snapshot of your financial habits.

1. Payment History (35%)

This is the biggest piece of the puzzle. Lenders (and landlords) want to see if you’ve paid your bills on time in the past. Late payments, missed payments, or anything sent to collections can seriously hurt your score. On the flip side, a solid history of paying on time shows you’re responsible and dependable.

2. Amounts Owed (Credit Utilization) (30%)

This looks at how much of your available credit you're using. Say you have a credit card with a $1,000 limit and you’ve charged $900, that's a 90% utilization rate, and that’s not great. Keeping your balances low (under 30% of your limit is ideal) shows you're not over-relying on credit, which boosts your score.

3. Length of Credit History (15%)

The longer you’ve had credit, the better. It demonstrates experience and gives more data for scoring. Even if you’re not using an old credit card, keeping it open (if there’s no annual fee) can help your score by increasing your average account age.

4. Credit Mix (10%)

Credit scores also look at the types of credit you have like credit cards, student loans, auto loans, or a mortgage. Having a healthy mix shows you can handle different kinds of debt responsibly. But don’t worry if you only have one or two types; it’s not the biggest factor.

5. New Credit (10%)

Every time you apply for a new credit account, it can cause a small dip in your score for a short time. Too many applications in a short period can make you look risky. But one or two new accounts won’t hurt much, especially if you manage them well.

Can You Rent an Apartment with Bad Credit?

Yes, renting an apartment with bad credit is possible, but it can be more challenging. Landlords typically use credit scores to assess financial reliability, so a low score may raise concerns about payment habits.

How to Get Approved with a Low Credit Score?

A low credit score for apartment approval doesn’t have to be a dealbreaker. Let’s find out the best ways to rent an apartment.

1. Be Honest and Communicate Proactively

One of the best things you can do is be upfront about your credit situation. Don’t wait for the landlord to find out, bring it up early and explain why your score is low. Maybe you had medical bills, a tough financial period, or just didn’t build credit yet. Being honest shows maturity and responsibility, and it may earn you some flexibility from the landlord.

2. Offer a Larger Security Deposit or Pay Rent in Advance

Money talks. Offering a bigger security deposit or a few months of rent upfront can ease a landlord’s worries. It shows that you’re serious, financially prepared, and less risky, even if your credit score doesn’t reflect that yet.

3. Provide Proof of Stable Income

Landlords care a lot about whether you can pay rent on time. If your credit score is low but your income is solid, make that the focus. Bring pay stubs, tax returns, or bank statements to prove your income is reliable. A strong employment history can help balance out a weak credit report.

4. Use a Cosigner or Guarantor

A cosigner (or guarantor) is someone, usually a family member or close friend, with good credit who agrees to back your lease. If you miss a payment, they’re responsible. This gives landlords added security. Just make sure your cosigner fully understands the responsibility before signing on.

5. Show Positive Rental History & References

If you’ve rented before and always paid on time, make sure to highlight that. A positive rental history can carry a lot of weight. Ask previous landlords or property managers for written references. This proves you’re a responsible tenant.

Check your tenant screening report before applying and fix issues that could hold you back.

Not Sure If Your Credit Is Good Enough?

6. Get a Roommate (with Stronger Credit)

Sometimes teaming up makes all the difference. If your roommate has a higher credit score, their profile can balance yours out. Plus, sharing rent makes things more affordable, which can look better to landlords reviewing your application.

7. Seek Apartments with Flexible Requirements

Not all landlords or property managers have strict credit policies. Smaller, privately owned apartments or individual landlords are often more flexible than large apartment complexes. Look for listings that mention "no credit check".

8. Write a Renter’s Explanation Letter

A personal letter can go a long way. Use it to explain why your credit score is low, what you’ve done to improve your finances, and why you'd be a reliable tenant. Keep it honest, positive, and professional. It adds a human touch to your application.

9. Demonstrate Other Strengths

Credit score is just one piece of the puzzle. Highlight your other strengths, like a steady job, savings in the bank, or a long history with one employer.

10. Set Up Automatic Payments

Offer to set up automatic rent payments through your bank. This highlights that you’re committed to paying on time and helps build trust with the landlord. Plus, it removes the risk of missed payments due to forgetfulness.

Common Mistakes Renters Make with Credit Checks

Many renters don’t realize how certain credit-related missteps can hurt their chances of getting approved for an apartment.

1. Not Checking Your Credit Report

Applying for an apartment without reviewing your credit report is awful. It’s important to know what landlords will see. Looking at your report in advance gives you a chance to spot any surprises, understand your score, and prepare to explain anything that might raise questions.

2. Ignoring Report Errors and Inaccuracies

Credit reports aren't always perfect. They can contain outdated accounts, incorrect balances, or even someone else’s information. These mistakes can lower your score and create a false impression of your financial situation. Taking the time to review and correct errors can improve your creditworthiness and help you get approved more easily.

3. Failing to Communicate with Landlords About Negative Marks

Staying silent about past credit issues often leads to rejection. Landlords appreciate renters who are transparent. Negative marks like late payments or collections, don’t always mean an automatic no. Taking the initiative to explain what happened and how you’ve improved shows responsibility and earns trust.

4. Skipping Verification of Income and References

Strong income and solid references can balance out a low credit score. But some renters forget or delay gathering this documentation. Without it, landlords may not have enough information to approve the application. Having your recent pay stubs, employer info, and previous landlord references ready makes your application stronger.

5. Not Disputing Outdated or Pandemic-Related Data

Old debts or pandemic-era hardships sometimes still appear on reports, even if they’ve been resolved. This kind of outdated information can make you look riskier than you really are. Taking steps to remove or update that data can improve how landlords see your financial situation today.

6. Submitting Unofficial or Doctored Reports

Some renters try to send altered credit reports or unofficial versions downloaded from third-party sites. This can damage your credibility and might lead to automatic rejection. Always use reports from trusted sources, and follow the proper application process.

7. Not Disputing Erroneous Eviction or Criminal Records

Inaccurate eviction or background records can seriously affect rental approval. These records don’t always belong to you, or they may have been resolved long ago. Taking action to clear up any wrongful or outdated entries helps ensure landlords aren’t basing decisions on incorrect information.

8. Neglecting to Follow Up After Denial

Getting denied for an apartment can be discouraging, but it’s also a chance to learn and improve. Many renters move on without asking why. Following up allows you to find out what went wrong, correct any issues, and approach the next application more confidently and prepared.

Final Words

In conclusion, knowing what credit score is needed to rent an apartment can help you plan ahead and avoid any surprises during the application process. For further guidance on navigating leases and managing rental agreements, LeaseRunner offers tools that can make the process simpler and more streamlined for both renters and landlords.

FAQs

Q1: What credit score do apartment complexes look for?

Apartment complexes typically look for a credit score of at least 620 to 650, though this can vary depending on the landlord or property management company. Some may accept a lower score with a higher security deposit or a co-signer, while others may require higher scores for premium properties.

Q2: What's a good credit score for an apartment?

A good credit score for renting an apartment generally falls between 700 and 750. With a score in this range, you are more likely to qualify for favorable lease terms, lower deposits, and quicker approval.

Q3: Does applying for an apartment affect your credit?

Yes, applying for an apartment can affect your credit score. Most landlords perform a hard inquiry when checking your credit, which may cause a small, temporary drop in your score.

Q4. Do You Need Credit to Rent an Apartment?

While having a credit history makes renting easier, it’s not always required. Some landlords and property managers are willing to rent to tenants without a credit score, especially if they can provide alternative proof of financial reliability.

However, corporate-run apartment complexes often require credit checks, so renters without credit may need to seek private landlords or explore alternative approval methods.